![[Workiva + Adra]: An Integration Powered by FHB](https://blog.fhblackinc.com/hubfs/Blog%20Images/Workiva_Adra/workiva_adra_featured.png)

[Workiva + Adra]: An Integration Powered by FHB

- Jamie Black

- Workiva

- minute(s)Adra is a leading software for the automation of the financial close process, while Workiva offers a cloud-based, collaborative platform connecting reports and data. Both solutions are known to save users time and money while improving accuracy and repeatability. And together, they equal more than the sum of their parts. FHB recognized that the combination of Workiva and Adra would offer a uniquely transparent, accurate, and controlled solution for financial close and statutory and regulatory reporting, while streamlining workflow across the entire record-to-report (R2R) process. So, we developed an integration tool to bring you the best of both worlds. Introducing: [Workiva + Adra] At FHB, we have one focus—streamlining and automating processes to lighten the workload of public sector finance and budget teams across North America. To that end, we partner with industry-leading software companies, providing custom implementation of the best available solutions to meet our clients’ needs. Workiva and the Adra Suite of Solutions by Trintech are two such valued partners. Learn more about [Workiva + Adra]. To find out how [Workiva + Adra] can work for you, schedule a call with our expert team. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Reap the combined benefits of Workiva and Adra with FHB's integration tool.

READ MORE

City of Albuquerque

- Rachel Raymond

- Success Stories

- minute(s)Collaborative ACFR Process Takes City of Albuquerque to New Heights Project: ACFR Automation Organization: City of Albuquerque Population: 562,599 (2021) Solution: Workiva Wdesk & Wdata The Need When we met the finance team at the City of Albuquerque, New Mexico, preparation of their Annual Comprehensive Financial Report (ACFR) was highly manual and time-consuming. “We [entered] our adjusting journal entries in PeopleSoft, [our] ERP system...[and uploaded] them…daily, sometimes twice a day,” said Mari Hughes, the city’s Deputy Controller. “When I first started, we combined hundreds of Word and Excel files, manually paginated all of them,” said Jason Shaw, CPA, Associate Controller for the city. Mari and Jason wanted “...something more user friendly and integrated, [that was] non-relational, column based," he said. Another pain point was “not knowing how to fix certain items when they [came] up, having to rely on technical calls and help just to resize a chart, things like that,” said Jason. “If there was an issue...with a formula or something, really, it was only me who knew how to troubleshoot it,” Mari added. While the Albuquerque team appreciated the power and capability of their legacy software, its limitations for their purposes made them realize that it might not be the ideal fit for their organization. “We used to create mirrored duplicate statements in Excel to check ourselves against [our software]” said Jason. The team struggled with the unfamiliarity of their existing user interface and some of its grouping concepts. Additionally, their software limited collaboration. Because it wasn’t cloud-based, and the finance team was assigned a limited number of user licenses, only one single person could work within a document at any given time, while their colleagues had limited, read-only access. When Albuquerque connected with FHB, they were seeking a more efficient, collaborative, and intuitive solution and overall process for producing their ACFR. The Solution The FHB team worked closely with Mari and her staff to assess their current process, then recommended implementing Workiva’s cloud-based tools. Wdata would serve as a central database and single source for all data, while Wdesk would be used for reporting and formatting. Unlike the custom syntax of their existing software, which was unique to their organization, the syntax in Workiva is mostly familiar to anyone who has used Excel, making the transition to Workiva much easier and more intuitive. In terms of groupings, the FHB team would be able to leverage Albuquerque’s existing groupings (already set up in their ERP) with minimal modifications. And as a cloud-based solution, Workiva would allow several of the city's team members to work within a document simultaneously. The Implementation A Uniquely Qualified Team The implementation took 16 weeks from start to finish. FHB Principal Consultant Christine Gilbert, CPA, CA, led the project. “She did a fine job of doing as much as she could with our data,” said Jason. Steering the team away from creating new, massive, complicated codes, “she was the one who just kept coming back to, ‘use what you already have.’” “I think you guys were really easy to work with, very clear and concise in expectations, from the client and yourselves.” –Mari Hughes The Albuquerque team also appreciated Christine’s unique combination of expertise in both their legacy software and Workiva. “She holds a very interesting seat, helping people implement both of them,” said Jason. Christine also demonstrated methods used effectively by other clients so that the city could pick the right approach for their needs. “The level of knowledge and detail and thoughtfulness about our data and how to make it work best was great.” –Jason Shaw, CPA All the Automation The FHB team was dedicated to making Mari and her team’s lives easier by automating as much of the ACFR preparation process as they could. While figuring out how to set up sheets in Workiva efficiently, Christine helped develop solutions for cash flows, based on how the Albuquerque team’s data works and how they had done them in the past. FHB also worked with Mari to balance her government-wide statements. Keeping Things on Track Mari’s staff was also pleased with how seamlessly the project was managed through FHB’s project management tool, Asana. “We would start every…meeting by ticking off tasks…the communication process and tagging people, that worked [smoothly],” said Jason. The Outcomes Time Savings One clear benefit of the city’s Workiva implementation is time savings. Their team will no longer need to create duplicate statements and publish multiple versions simultaneously. “The way that Christine worked through...the implementation should virtually eliminate a lot of the mirrored work that we were doing.” Jason said. Workiva’s grouping functionality will save the city even more time. “We were able to leverage the attributes that we have in our ERP system, which we implemented…with the intent that we were going to use those for our grouping codes…the implementer for [our former software] told us we couldn't use them. But for Workiva, we're able to use them…now [we won’t] have to spend a bunch of time each year…grouping new things,” said Jason. “It's going to save some time, particularly on the more detailed schedules...it could save one to eight hours per the big funds, particularly if you've got a lot of new data,” he said. Freedom to Do More Mari is excited about using the time they’ll save to focus on higher-level tasks. “The way that we've got the citywide statement set up in Workiva, with the linking and things like that…if there [are] any issues with the reconciliation…those will be easier to identify,” she said. “And I don’t have to worry about any inconsistency there...that's going to save some time. And then I think that will hopefully free us up to do a little bit more thorough...final review.” “A repeatable process is what we're looking forward to the most—being able to teach... more than just Mari and I...how to do the critical functions,” added Jason. Ad Hoc Reporting The team is excited to be able to capture and share a true snapshot of accurate data upon request. Enhanced Collaboration Mari's team can't wait to take advantage of Workiva's cloud-based environment, where multiple people can view the data and make updates at the same time. They will no longer need to rely on screen sharing to demonstrate how to fix something, for example. “We're extremely grateful for the collaborative workspace that this will be.” –Jason Shaw, CPA Ease of Use Because working in the Wdesk report writer is like working in a beefed-up combination of Word and Excel (with which her team is familiar), Mari will no longer be the sole troubleshooter on staff. “I think it’s just more straightforward,” she said. Mari added that her team looks forward to using Workiva for report formatting, as “there’s not going to be that kind of fighting with it,” that they experienced previously. “Things like that, I think are going to make our lives a lot easier, because you don’t need to be dealing with that stuff when you're in the eleventh hour, and you're already freaking out about deadlines. And then you have a software program that's just not that easy for you to use,” she said. As icing on the cake, Mari has found the Workiva support and training site to be thorough and easy to use, she said. Looking Ahead More Hands On-deck In the past, Mari and Jason were the only team members capable of data review. “We haven’t felt comfortable [sharing the review] because…[neither of us had] time to explain more,” to staff members who expressed interest in helping. “It was, ‘thank-you, but no’,” said Jason. “At this point, I think we're going to be able to start opening some of that up as well…keeping the two of us on…the overall picture instead of the minutia of…rounding from front to back. We can let some of the other more advanced staff do things like that, [which] we weren't comfortable with before,” he said. Spreading the Word Since the implementation, Mari has become an FHB advocate. “I've already told a couple people…like my former boss…she's got a different agency now…I told her…we're going to Workiva and she [said], ‘Oh, how are you liking it so far?’ I said, ‘so far, I like it much better’…I was telling her…about being able to leverage our groupings that already exist and [such]…she [is] hoping to look into that within the next couple of years [for herself]. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

With help from FHB, the City of Albuquerque traded hundreds of manually manipulated Excel and Word documents with erroneous links for an efficient cloud-based, purpose-built solution for preparing its ACFR, resulting in saved time and effort.

READ MORE

School District 83

- Rachel Raymond

- Success Stories

- minute(s)Time to Focus on the Big Picture: Automating Financial Statements for School District 83 Project: PSAB Automation Organization: School District 83 Students: 6,100 Platform: Workiva The Challenge The finance team at School District 83 (Okanagan-Shuswap, British Columbia) was looking to save time and money; reduce errors; and improve its reporting reliability, repeatability, and standardization; by automating its financial statements. When we met the team, their data preparation stage was heavily dependent on complex spreadsheets—requiring too much keying and leaving little time for analytics. “We utilized Excel, as well as other Office products—like Word for our financial notes and our financials, even discussion analysis. So, it was a very fractured overall process when we...look back on it,” said Jeremy Hunt, Finance Director for the district. The team was accustomed to finalizing, formatting, and preparing statements manually—a time-consuming and frustrating process. Additionally, they were required to complete Local Government Data Entry (LGDE) forms, which meant replicating the information from their annual report and manually keying it into the ministry’s template for online submission. Jeremy explained that in previous years, the team's work was paper-heavy. "We have binders. Nine-inch or 12-inch binders. I know they’re massive for year-end. And the backs of those…are all printed and messy,” he said. What’s more, the finance team frequently had difficulty finding original hard-copy source documents to back up their data. Jeremy looked forward to updating their process, so they “wouldn’t have to find a paper copy every year…that validates a number.” The district’s team also wished to collaborate simultaneously without risk of overwriting crucial information. “We wanted something that allowed access to the individual that was required to do that work, but locked down areas where we didn't want them working,” said Dale Culler, Secretary–Treasurer/CFO. They were also interested in a multi-functional tool. “The biggest limitation that we have in our department...is staffing resources to move forward with any initiative...and when we consider the end product, we wanted to move towards something that would allow us to potentially consolidate...future reporting requirements,” said Jeremy. The Solution FHB met with the district’s team to evaluate their existing processes and develop a customized solution to meet their needs. Initially, the conversation included using Caseware. “The Caseware discussion was because that's what we...were familiar with. But we also wanted to be open, to hear about advancements in the industry, where it's going...Caseware requires a very specific knowledge. We wanted something with the structure, the rows and columns that people are familiar with,” said Dale. In the end, FHB recommended Workiva. As a cloud-based platform, Workiva offers a collaborative database (Wdata) as a single source for data entry/management and an advanced report writer (Wdesk) for instant and automatic preparation of consistent, formatted reports—mitigating risk of data-entry and calculation errors and improving overall report accuracy. "It was concerning that it would be difficult to learn a new piece of software. But once we got into it and started to see the back end of it and how it really worked, and became more familiar with it, it was very Excel-based. That took away a lot of the reservations that I had, and I believe Dale had as well, about us being able to understand and use it in a logical manner that would follow what we're used to,” said Jeremy. The Service “Christine was on top of it. She kept us on the tracks…I can’t say enough about what she did for us. She’s very helpful.” –School District 83 Finance Director Jeremy Hunt Throughout the project, the School District 83 staff was highly impressed with the responsiveness of the FHB team. [FHB Principal Consultant Christine Gilbert, CPA, CA] did a great job…she would answer questions whenever I would throw them over, and…usually it was within like an hour,” said Jeremy. “It was a great experience.” “It's definitely appreciated that Christine had some experience in PSAB that we could draw support from,” he added. When asked to rate FHB’s general knowledge of Workiva and reporting standards on a scale of one to 10, with 10 being “the greatest ever,” Jeremy responded, “It’s a nine or a 10.” He wouldn’t hesitate to recommend FHB to peers and colleagues. “They were patient when we were struggling to keep up…they were accessible and worked with us on issues that we had…I would definitely recommend that FHB would be a good partner to implement any accounting-related software.” –Jeremy Hunt The Results So far, the greatest benefit of the Workiva implementation has been time savings. “It's just going to reduce the amount of…data entry that we have historically relied on. We were using reports from our old clunky system that doesn't provide great reporting…mapping was not the greatest previously. So, it's...going to speed up that manual entry time. It will help us validate data as well,” said Jeremy. Jeremy added that Workiva has far exceeded his expectations. “User friendliness has been amazing...it didn't take much training, to be honest, to understand how to use this product...on top of that, I can see how it links everything together and can easily produce something that is better than what we have previously done over many hours—in just an hour,” he said. Dale agreed, adding, “Workiva provides one place...in which to do review...and because it's very consistent with the way that we've been trained to look for things when...creating working papers, it'll be much quicker to do that." Before Workiva, "when things were disjointed...I’d have to interrupt...Jeremy...stop his workflow, so that he could show me where things were. In the new platform, I can just look at the progress of the review as it is...I don't have to wait for it to be finished; I can look at it live,” he said. Looking Ahead In light of this project’s success, District 83 has decided to move forward with two additional projects. “So…the bigger one is going to be the budget…we want to integrate our budgeting into Workiva,” said Jeremy. “We’re thinking next year, maybe toward the end of 2023, into 2024.”“...After this audit season, we’ll look at financial reporting quarterly…at some point maybe move into monthly statements,” said Jeremy. “Quarterly reporting is probably the next logical step...before we even do the budget,” said Dale. With all of the time they’ve saved, Jeremy looks forward to taking on higher-level tasks. “I'm fairly production-based right now in my job as a director, whereas I need to be more focused on oversight and the bigger picture,” he said. The District 83 team is pleased with how far they’ve come, and optimistic about the future. “We’re just scratching the surface of what Workiva can do for us,” said Jeremy. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

School District 83 wanted to improve and standardize its PSAB reporting process, making it more reliable, repeatable, and faster without increasing resources. They achieved that and more with the help of FHB.

READ MORE

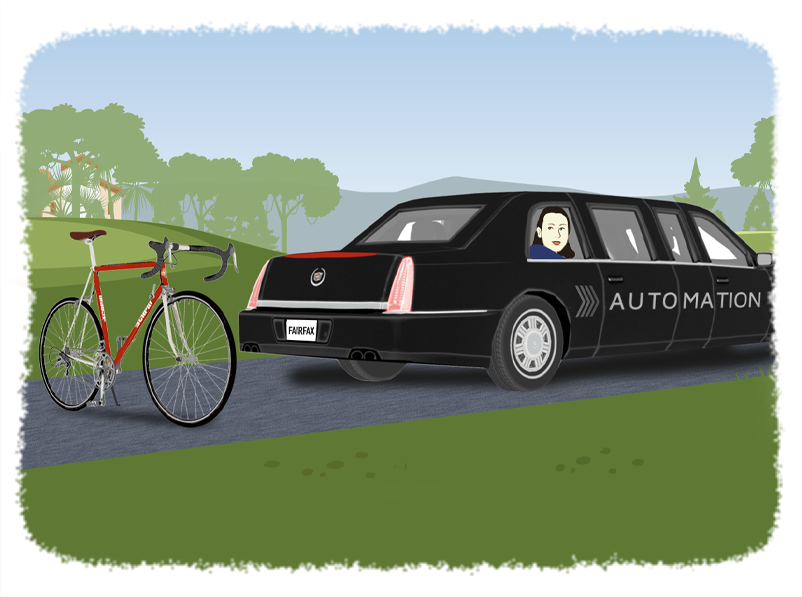

Fairfax County ERFC

- Rachel Raymond

- Success Stories

- minute(s)Riding in Style: How ACFR Automation Changed the Game for Fairfax County ERFC Project: ACFR Automation Organization: Fairfax County ERFC Established: 1973 Solution: Workiva Wdata and Wdesk The Challenge For the staff at Educational Employees' Supplementary Retirement System of Fairfax County, Virginia (ERFC), preparing and publishing an Annual Comprehensive Financial Report (ACFR) was a tedious process. Multiple people were tasked with entering data and repeatedly checking each other’s work. If they changed a figure in one place, they had to manually update it in a number of other places. Allison Kelly, CPA, Senior Retirement Financial Analyst at ERFC, explained, “We have had three people working on the table of contents, reviewing it. Because we've changed things, now we have to re-review [it] … we have spent hours with … communications folks … double checking the table of contents … just that is … a day's worth of work.” Fatigued by the process, Allison broached the subject of automation with her executive director. “We were talking about the painful process we had for doing the ACFR and I said … we could get software to do this … and he said, 'Find out! Go—go do it.'” –Allison Kelly Allison began researching available solutions and polling fellow finance teams for recommendations. “I had heard from a few systems that, you know, it's painful, the conversion is painful … so I was geared up for this, this pain...” The Solution Ultimately, Allison connected with the team at FHB, who carefully reviewed ERFC’s needs, then weighed workable solutions. FHB recommended adopting Workiva’s Wdesk and Wdata. As cloud-based software, Workiva would allow multiple users to work on the ACFR simultaneously. As a single-source database-driven system, it would eliminate the need for a variety of disconnected spreadsheets. And its formatting automation would make report finalization and publishing a breeze. A Painless and Effective Implementation Once Workiva was selected, a dedicated FHB project team guided the Fairfax staff through the software’s implementation, customizing the solution to fit their unique needs. Allison was pleasantly surprised by the smoothness of the conversion. “… I mentioned to [FHB Principal Consultant Christine Gilbert, CPA] and [FHB Principal Consultant Amy Manthey, CPA] a few times, am I missing something? Because I'm still waiting for this other shoe to drop, and I'm not feeling that pain. I don't know if it was them. I don't know if it was me … but … that … was not my experience at all.” “And for us, you know, our ACFR process kind of went from riding a bicycle to … driving a luxury vehicle … it was already great. But that just made the road so smooth.” With the help of FHB, Allison and her team grew “very comfortable” working in Workiva. “Everything works just the way it’s supposed to,” she said. Her staff found Asana, FHB’s project management tool, to be user-friendly as well. “I loved how all I had to do was drop a comment in the sheet or whatever I was working in. And then Christine or Amy would just reply to the comment.” This convenient functionality eliminated the need for additional emails, phone calls, and meetings. “I really, I have no complaints. I thought the way the project was run was just … so well done, that it made my job a lot easier.” The Results For Allison’s team, one of the greatest benefits of the implementation so far has been time savings. “I think it is 110 percent a timesaver. 110 percent we’re already benefiting. I mean … we're already working on our ACFR for next year. And … that's not something we would have done in the past … we got through phase one, we did our ACFR, and then we got through phase two. And now, there's so many more improvements we can do and efficiencies that we can put into it … I have time now to work on those…” “I'm really grateful we have it. I'm glad that … the project was able to happen and that it's done for the most part, because it really is a game changer.” “If I'm going to quantify what our actual process used to be, compared to what it's going to be now, [the time savings] is absolutely in the weeks—could even be a month.” To be clear, that’s a month’s time for many staff members, not just Allison. “We get our final numbers at fiscal year-end, and there's going to be maybe 20 percent of the work to do because 80 percent of it is done up front.” Looking Ahead In light of their ACFR project’s success, there has been some discussion about whether the county of Fairfax (as a whole) might benefit from an FHB-led Workiva implementation for their budget book process. FHB Client Services Manager Rachel Raymond and Wendy Zhi, CPA, Acting Deputy Executive Director for ERFC, have plans to follow up. When asked if she had any complaints about the FHB project team, Allison joked, “Yeah. That I don’t get to see them every week anymore … I feel like we have [a] good thing going, you know, new friends, … and now it's like, I don't get to see them anymore…” © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Read how Fairfax County ERFC saved weeks of work by partnering with FHB to optimize their ACFR process.

READ MORE

Discovery as a Foundation for Success

- Jamie Black

- Best Practices

- minute(s)Why Is Discovery Such a Crucial Step? Discovery sessions are key to ensuring that a project will result in the desired outcome for our clients, our partners, and ourselves. They provide a forum for all stakeholders to build a common understanding of the challenges of the current processes and tools; the needs that must be addressed by the solution; project objectives; and potential hurdles and pitfalls. A productive discovery session resolves misunderstandings and sets the tone for open, clear, and consistent communication. It is a critical first step to ensuring team buy-in and is essential to maximizing the benefit you receive from the project. Learn more about managing change. How Can We Ensure a Fruitful and Effective Discovery Session? Have the right people in the room. First and foremost, you must include those in the trenches who perform the process. The more people with this perspective you can include, the better. Only they can offer an intimate look at process details; practical feedback regarding shortcomings, nuances, and time involved in the current approach; and a thoughtful wish list of essential features in a new solution. They will ask the right questions, and their answers will provide invaluable insight. Next, be sure to include senior management and the business process owner(s). These are the people who understand the big picture—e.g., political implications, budget and time constraints, your organization’s vision, and overall goals. They can speak to how process challenges impact the execution of your organization’s strategy. Be completely candid. It’s important to make the discovery session a safe place to voice concerns and provide honest feedback, even if the conversation becomes uncomfortable. Are you short-staffed? Is your team relatively inexperienced? Are they lacking technological savvy? The more we understand your true challenges, the better we can design an implementation plan to tackle them. If We Don’t Include the Right People, What Could Go Wrong? In a word, everything. Without the right people in the room, you risk wasting countless hours, and losing hundreds of thousands of dollars. Failing to reveal key considerations up front can lead to process gaps you may not have the budget to fix. You might end up having to change or shrink the scope of your project. You might have installed the wrong software and be forced to start over. Worst case scenario, your implementation could result in complete failure. After all, a whopping 70% of IT projects fail. Change management research has revealed that making a decision about a significant change without input from your whole team will likely engender frustration and resentment, creating project adversaries instead of advocates. If We Prioritize Discovery, What Could Go Right? When all stakeholders have a voice in discovery and project goals are on target, everyone wins. As the US Navy Seals say, “Slow is smooth, smooth is fast.” When you focus on conducting each step of the implementation—starting with discovery—correctly and completely, you will see your desired results more quickly. In the words of our President, Jamie Black, “Take your time. Do it once, do it right.” "I have been involved with this kind of software implementation system upgrade for many, many years...when I started to go through the procurement process, I could never imagine it would have gone so smoothly, with this level of success." -Dongmei Li, Assistant Controller–Corporate Accounting at Chicago Public Schools © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Learn why discovery sessions are so important, who should attend, and what should be discussed.

READ MORE

Change Management: An Introduction

- Jamie Black

- Best Practices

- minute(s)Key Considerations for Managing Change The way our clients react to change and their level of change acceptance can influence their success as much as their budget, choice of software, or technical aptitude. How do we know? We’ve been helping public sector finance and budget departments across North America improve and automate their most time-consuming and tedious business processes for nearly 30 years. So, we thought it might be helpful to share highlights from research behind the importance and key features of change management. What Is Change? Change is both the process through which something is made different (a verb) and the result of that process (a noun). The adaptation, growth, and very survival of human beings has long depended on our ability to manage change. Consider the crucial advent of fire-building or weapon-making, or the more contemporary prerequisite of technological savvy for success in the modern workplace. Organizational Change Change management within an organization involves the activities, functions, and tools it uses to deal with something new. As an example, institutions of all kinds use the tools of training and development to ensure their employees’ sustained competence and efficacy amid the ever-changing dynamics of the workplace. Global research and advisory company Gartner reports that today’s average organization has undergone five significant organizational changes in the past three years—and almost 75% of those expect to expand major change initiatives over the next three years. Change initiatives range in scope and complexity from process improvements to mergers and acquisitions. Timeframes for organizational change can range from slow and gradual, like rethinking each individual step in a process over time, to quick and total, like suddenly adopting an entirely new system or approach. As with individuals, an organization’s ability to survive, stay relevant, compete, grow, and last, depends on its ability to manage change—both internally and externally. WANT TO LEARN MORE? In his 1996 book, “Leading Change,” John Kotter was among the first to apply the academic theory of change management to the world of business. His eight-step change management process remains relevant to this day. Other notable change management models include Lewin’s Change Management Model, and Prosci’s ADKARⓇ Model Change Is Difficult Despite the inevitability of change, people (by nature) prefer stability over anything new or unfamiliar. Known as cognitive bias, this tendency is thought to be an unconscious process, whereby people cling to a belief system despite being presented with a better solution. DID YOU KNOW? One 2019 study found that monkeys (capuchin and rhesus macaques) were “significantly more likely to adopt new and more efficient shortcuts to attaining their goals than humans.” The McKinsey consulting group reports that 70% of all change initiatives fail. The reasons for failure include: Misalignment of values reflected in the change itself and values of the people experiencing the change Failure to manage employees’ attitudes toward change Lack of awareness of change’s potential benefits Change is seen as unfair or punishment Staff members may fear: A shift in duties Losing their job to automation Revealing weakness/incompetence in technology or role Loss of control Ripple effects More work An unrealistic timeline or insufficient employee participation in training can further hinder the success of a change initiative. Unsuccessfully managing a workforce through change can be costly; dissatisfied employees are known to be less productive and are more likely to leave an organization. The development of negative attitudes and adverse reactions toward change is known as resistance to change. Research suggests that employees’ readiness for change strongly influences their resistance, by transforming their attitudes. In other words, change is more successful when employees are prepared for it, not surprised by it. DID YOU KNOW? The Society for Human Resource Management (SHRM) has identified six states of change readiness: indifference, rejection, doubt, neutrality, experimentation, and commitment. Change in the Public Sector Is Especially Difficult Government entities are typically slower to accept and adopt changes—like the introduction of new technology or business processes—than organizations in the private sector. Reasons include: Less funding Higher public scrutiny Lack of internal informational technology (IT) staff or capacity Siloed duties and departments Complicated contract processes For some public sector organizations, slow adoption of technology and process change has led to more expensive and burdensome service provision. When they embrace change, they: Help eliminate time-consuming, frustrating, and “glitchy” processes Can focus on the actual work of providing services Make their staff more accessible to the public Get help more efficiently to those who need it The benefits of change in the public sector are clear. The challenge is that government employees may be among the least comfortable or familiar with change. Consequently, greater change management support is likely necessary in those settings. To Be Successful, You Must Manage Change The Importance of Leadership Both a systematic approach (strategy) and effective leadership are critical to the success of any organizational change endeavor. A change management strategy provides leaders with steps to successfully guide an organization through change, while limiting disruption and unexpected consequences. The goal may be to change a process or approach, but the key to success is the ability to effectively lead people through the change. Keep It Human The fundamental common denominator among successful change initiatives is people. To effectively implement change, leaders must take its impact on people into account. The following steps can help garner stakeholder trust and promote acceptance (and even appreciation) of a proposed change: Clarify the desired end result in advance. Highlight pain points and the need for change. Make the change as specific as possible. Be transparent about its benefits and challenges. Listen to and address employees’ reactions. Establish their commitment to the initiative. Remember the study that found monkeys adapted to change more readily than humans? Turns out, when the benefits of using a new approach were made clear, “humans were more likely to get on board.” Why It Matters The importance and impact of effective change management cannot be overstated. Financial, cultural, institutional, and other factors make organizational change in the public sector particularly challenging. The right approach is vital to the success of any change initiative. Securing employee buy-in not only makes change easier, it establishes a relationship of trust, reducing resistance overall and minimizing the need to campaign for future reengagement and support. With the right combination of communication, preparation, planning, and support, a well-managed change can dramatically elevate both the quality of employees’ day-to-day experience and the focus of their work. Let Us Help Decades in the business of change have informed FHB’s successful approach to streamlining and automating even the most deeply ingrained and archaic business processes in the public sector. Schedule a meeting with us today to explore how we can help manage your organization’s need for change. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Learn about organizational change, why it's particularly hard in the public sector, why it's important to manage it, and how to do so effectively.

READ MORE

City of Knoxville

- Rachel Raymond

- Success Stories

- minute(s)City of Knoxville Reduces Budget Book Workload by 50% Project: Budget Book Automation Organization: City of Knoxville Population: 192,648 (2021) Solution: Workiva The Scenario & Solution The finance team at the City of Knoxville, Tennessee was spreadsheet-weary. They wanted a collaborative tool and a streamlined approach for creating their annual budget book. So, they engaged Workiva and FHB to automate the process. The Outcome Kittrin Smith, Deputy Director of Finance for the city, said she and her team were “very happy” with the project’s implementation and outcome. She estimates that the new solution has eliminated, “… at least 50 percent of our work on the production of the book." She added, “... that was always a heavy lift that multiple analysts had to work on. So, I definitely feel it was worth the time and money that we spent. [It’s a] very valuable asset … that we will continue to use every year.” “I feel like we’ve come out of the dark ages.” –Kittrin Smith, Deputy Director of Finance, City of Knoxville Since Workiva is cloud-based, many users can now work on the city’s budget simultaneously. And it’s database-driven, so instead of the staff spending countless hours manipulating data in multiple spreadsheets, the data flows in and is mapped all the way up to the budget book. “The ability to get more real-time data without having to start from ground zero again,” has made the team’s lift significantly lighter. In addition, Workiva’s advanced publishing capabilities make formatting easy, eliminating the need to manually modify the table of contents, page numbers, margins, fonts, and the like. "So, the software was a great help, it was a success. Everyone here on our side, all the way through the administration [and] mayor liked it.” What's Next? Kittrin will work with FHB support to continually refine and enhance the solution. She is considering expanding its use to prepare mid-year and other reports. “We already have a few things that we want to tweak going forward.” Throughout the budget book project’s implementation, the city was short-staffed, relying on an outside consultant to lead the process. Kittrin is hopeful that they will soon be able to hire a dedicated staff member to manage future projects. “I’m really looking forward to the time when we have a staff member, who … takes the lead with the software and how we use it. That's really going to enable us to expand the use of it,” she said. With the city’s new documented and repeatable processes in place, any new team members will be able to step in and get up to speed more quickly. Since the Knoxville team had such a positive experience with FHB’s Director, Solutions Design and Architecture Darryl Parker, CPA, CMA, who led the project, they hope to partner with him for the next stages of implementation. “Darryl is very knowledgeable, very helpful. It would be nice to be able to work with him again.” © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

With the help of FHB and Workiva, the City of Knoxville reduced their budget book preparation workload by half.

READ MORE

ERM Toolbox – How to Develop Risk Appetite/Tolerance Statements

- Ed McCaulley

- In Control

- minute(s)Risk Appetite and Risk Tolerance Statements One of the key steps in developing an organization’s enterprise-wide risk management (ERM) framework is establishing written statements regarding its risk appetite and tolerance. These statements serve as guideposts to help employees make both strategic and tactical decisions; thresholds for risk metrics; and benchmarks for assessing whether the organization is comfortable with its own risk profile. They are vastly important. So, who should be involved in developing them and what does that process look like? As discussed in the first blog in our ERM Toolbox series, "Why Do I Need Risk Appetite and Tolerance Statements?, establishing an organization’s risk appetite and risk tolerance statements is a vital step. Once an organization has seen the light and made the business case for setting these guidelines, the follow-up question is, “How are these statements developed?” For an organization that has not yet defined its risk appetite and risk tolerance statements, this question can seem intimidating. So, I’ll break it down into three smaller questions: 1. Who should be involved in developing the statements? 2. What is the best way to elicit information from participants? 3. Who should be involved in approving them? STEP 1: DECIDING WHO SHOULD BE INVOLVED Invitees to the party usually include the organization’s top level of management—AKA its executive team, senior leadership, or C-suite. This core group of individuals is going to be most familiar with and responsible for achieving the organization’s mission and strategic objectives. Add to this group any subject matter experts that provide necessary insight into certain risks that the organization faces. If an individual’s voice must be heard, either because they are instrumental in achieving strategic objectives or they manage the mitigation of a key risk, invite them. Lastly, include members of the risk management group—whether they’re assigned to a formal, independent risk management function or given ad hoc responsibility. As a pragmatic concern, the group should not be too large as it is harder to develop consensus with larger groups. Up to 12 members should suffice. STEP 2: DRAFTING THE STATEMENTS Theoretically, risk appetite and risk tolerance statements could be drafted and agreed upon through an iterative series of questionnaires or through software that allows for deep collaboration. However, in my experience, a workshop is the most efficient way. Methods may be dictated by what you are hoping to achieve, namely a consensus on which risks are acceptable and which are not. Running a Risk Appetite & Risk Tolerance Workshop Workshops do present their own challenges. However, participant training, competent workshop facilitation, and clear workshop objectives will help address those challenges. Many of the following steps might seem self-evident, but my advice for holding a successful workshop is as follows: 1. Schedule it so that everyone can participate. This is easier said than done, as these people are BUSY! 2. Ensure all participants know what is expected of them during the workshop—as workshop participants and as a group. This can be handled simply by providing a meeting invitation that includes an agenda and location, and establishes workshop “rules” (e.g., no phone calls, texting, or email during the session). 3. Establish a base level of ERM concept knowledge for participants. Understanding of the terms risk appetite; risk tolerance; risk mitigation; and inherent and residual risk; as well as risk types, is important. This training can be provided separately but can be very effective if provided on the same day, ahead of the actual workshop. The goal is full participation from all workshop attendees, not just those who are “in the know.” 4. Request that all participants bring copies of the corporate policies for which they are responsible. For example, the treasurer might bring the banking policy and the CIO might bring the acceptable use policy. These policies often serve as a starting point for risk tolerance statements. 5. Consider hiring a professional facilitator. The facilitator’s job is complex; they must be mindful of assessment bias, prevent or negotiate conflict among attendees, dissuade individuals from dominating the conversation, and encourage participation by those inclined to be wallflowers. Knowing when to table a discussion and move on is also a valuable skill. Rabbit holes explored by just a few individuals can cause the larger group to lose focus. 6. If the number of workshop participants is large or is having trouble reaching consensus, consider using break-out sessions based on topic (e.g., risk type), then bringing recommendations back to the full group. 7. At the conclusion of the workshop, summarize outstanding items (there will be some), assign ownership, discuss next steps, and communicate a timeline. Follow up in a timely manner with an email to the participants, providing this same information. Ensure that each individual understands their required deliverables and timeline. 8. About a week after the session, reach out to participants to gauge their impressions of the workshop. Ask if they think the workshop was effective in building consensus around the risks the organization is willing to accept, those that it will not accept, and a delineation between the two. 9. Don’t seek perfection. There is no need for endless debate over each metric—like whether a 3, 4, or 5 percent ROI is ideal. It is natural that, like a new pair of shoes, these initial metrics may need to be adjusted. STEP 3: OBTAINING APPROVAL Obtaining approval of the risk appetite and risk tolerance statements is the “blessing” that puts them into practice. They then become the rulebook, the guidebook, the playbook for risk taking. However, the task of gaining approval may reveal additional risk threshold questions that must be answered by management. Organizations usually have some form of supervisory body on which approval of risk appetite and tolerance statements will fall. In a corporation, this is their board of directors. In a public sector organization, it may be their council. To prepare the board/council for this responsibility and to ensure everyone is in alignment with expectations, they should be given the same baseline ERM training as management. And management should be prepared to respond and adapt to the board/council’s oversight. CONCLUSION For an organization looking to define and publish their initial risk appetite and risk tolerance statements, the process can seem intimidating. However, involving the right individuals, holding an effective workshop, and seeking the right approvals, can make this process achievable. The key is to effectively channel senior management’s time to discuss, debate, and come to a consensus on enterprise-wide risk constraints. The clarity gained will equip employees to manage their individual risks and empower the organization as a whole to respond to risk more confidently and consistently. Read the first blog in our ERM Toolbox series. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Learn how to develop risk appetite and tolerance statements, who should be involved in drafting them, and tips for holding an effective workshop.

READ MORE

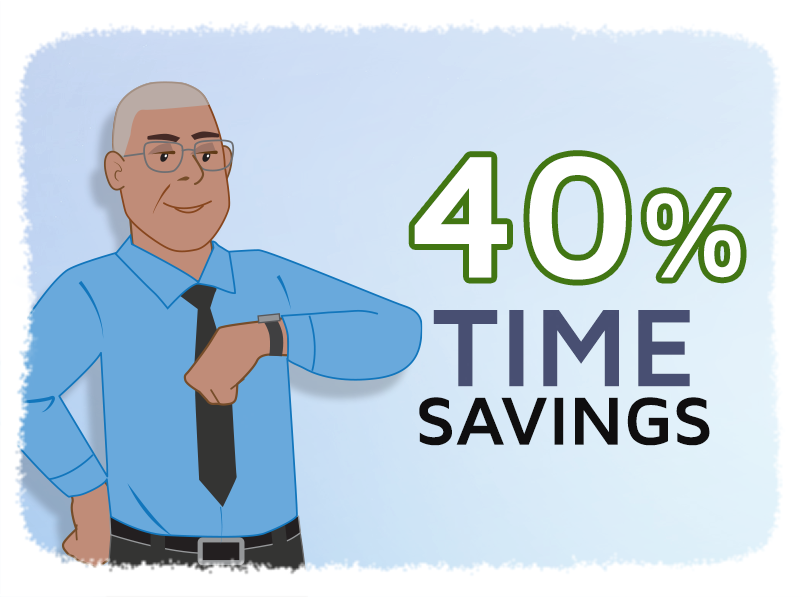

City of Torrance Sees a 40% Time Savings with Audit Management Project

- Rachel Raymond

- Success Stories

- minute(s)Automation Reigns in Southern California Project: Audit Management Organization: City of Torrance Population: 143,600 (2021) Solutions: Workiva Audit Management Software The Need While working on a project with Workiva, the finance department for the City of Torrance, Calif. expressed a desire to update their approach to Governance Risk and Compliance (GRC) and audit management. The Workiva team recommended connecting with a valued partner, FHB, for help. Our dedicated team assessed the city's existing audit management process—which was mostly manual, using Word and Excel—identified opportunities for improvement and automation, and made a recommendation to implement Workiva Audit Management software. The Solution One of the many features that set Workiva's audit management software apart as the best solution for Torrance is its flexibility. It adapts to users’ processes, rather than requiring the reverse. And it allows users to plan, test, report, and monitor their audit work in a single platform, eliminating the need for countless emails and files containing various versions and revisions. Its real-time dashboards put the data they need within reach, right when they need it. And it will automate repetitive tasks, evidence gathering, final engagement reports, and risk assessments. The Implementation Fulton Bell, senior auditor for the City of Torrance, describes working with the FHB team to implement Workiva as “very positive.” Fulton was impressed with the depth of FHB’s subject matter expertise and experience. It was clear that both Ed [FHB Principal Consultant Ed McCaulley, CPA, MBA] and Megan [FHB Principal Consultant Megan Soles, CPA, CA] had spent time in the field, sitting at a desk much like his, doing similar work. Having been involved in two prior, somewhat bumpy, software executions (SAP and Oracle), Fulton had braced himself for a difficult Workiva implementation. However, he was pleasantly surprised. “From my standpoint … working with Megan and Ed, they made it really easy.” “...comparing it to a couple of implementations I've done before... this was by far the best ... [FHB’s] knowledge was great.” For initial setup, Workiva’s audit management software required a one-time import of data—including control descriptions, risk descriptions, departments, people, audit issues, action plans, etc.—into its database (Wdata). Following initial setup, the Torrance team can modify data using forms customized by FHB. Internal auditors also use forms to capture work papers, findings, action plans, etc. FHB configured Workiva to meet the city's distinct needs. This included creating an input form for controls and changing the data model itself with instructions for field selection and type (text or date field, e.g.) In total, the FHB team set up eight different forms for the City of Torrance. Another feature of Workiva’s audit management software that will help Torrance is its planning module, used to develop an annual audit plan. It includes information such as which audits will be performed during the year, how many hours will be budgeted for each, which auditors will be included, etc. The Workiva audit management solution also features a real-time dashboard, so the city’s finance team can see a quick snapshot of audit project status, document requests, action plans, and the like. “The team at FHB was great. Ed had some very good ideas that we used to customize the dashboard. And based on her experience, Megan offered advice about how to best use particular fields. She gave us direction that was very helpful in building the audit information sheets.” Three of the main outputs requested by Torrance were the audit announcement letter, audit report, and internal audit status report. FHB developed various queries and customized spreadsheets to meet those deliverables and provided detailed documented instructions for using them. The team also put together a chart at the end of the internal audit status report that serves as an aging schedule, so that the city can better track its outstanding action items and audit recommendations. “The project went well … the implementation, the communication, meeting each week, going over the various steps, and working with us on any issues that we had, and trying to build the project … all of that went very well.” The Results For the City of Torrance, time savings is by far the greatest outcome of the Workiva implementation. Fulton estimates that their new process and software will cut his team’s work time by 40 percent. "It's going to save us a ton of time. It was a little bit of work on the front end ... doing it for the first time … trying to get the numbers to balance … I can see how much time is going to be saved going forward.” Fulton and his team are not only pleased with the amount of time they’ll save, they’re also grateful for the follow-up care provided by FHB. “Even after the close of the project, we appreciate the time that was given to help us through... we were able to come back and ask some questions and get some assistance.” Next Steps The City of Torrance has now identified additional ways to leverage Workiva. “Our whistleblower program is probably going to grow. [Our original project] was built around doing audits and not so much doing investigation. [So, we’re looking to] automate that side of it and see where we can use Workiva for that.” Fulton has received requests to do monitoring controls and work with external auditors. “Some of the more immediate next steps [are] to ... build a template for the fraud investigation side … and ... monitoring the various internal controls that we have implemented through some of the audits that we have done.” Another project on the horizon for the Torrance team is an accounts payable audit. They’ve already done all the internal controls but would like to establish a process for duplicate payments and other issues. FHB has suggested that Workiva’s audit analytics functionality (included with the audit management software that Torrance has already purchased) can help. The FHB team can script the solution so that it loads and tests data without any additional effort from Fulton’s team. With the time they’ve saved, the city has also begun to make audit reports accessible to the public on their website. “Saving that 40 percent [gives] us more time to ... handle some of the workload.” © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

The City of Torrance, California was seeking a new approach to audit management. FHB stepped in to help improve and automate their processes using Workiva Audit Management Software.

READ MORE

Workiva 101: Beyond the Basics

- Michelle Richardson

- Training

- minute(s)The Need Although Workiva offers excellent, basic training for beginning users as well as additional specialized courses, many of our clients have expressed a need for more. We created Workiva 101: Beyond the Basics to provide a space for more than simple skill-building. This training serves the broader goal of enhancing our clients’ understanding of the domain they work in. It will improve attendees' ability to participate meaningfully in conversations about data and report automation. Like the reporting standards (GASB, PSAB, FASB, etc.) themselves, Workiva’s functionality is changing all the time—so we aim to help our clients become nimbler, lifelong problem-solvers. The Difference Workiva 101 differs from other course offerings in a few ways. First, the course was designed with adult education best practices in mind. Pre-course and post-course surveys and a course assessment are included as part of the overall learning experience to maximize engagement and enhance learning outcomes. Rather than being solely lecture-based, the course includes interactive components at every step, promoting the retention of skills and the reasoning behind them. In addition to its instructional piece, the training features live demonstration of the skills discussed. And finally, Workiva 101 allows participants to practice the skills they’ve just learned in a hands-on, safe workspace, with real-time guidance and oversight from our expert instructors. After all, watching an instructional video doesn’t give learners confidence. Practice does. A New Mindset Many of our new clients are refugees from a land of spreadsheets, with a deeply ingrained reliance on manual data entry and manipulation. They’ve learned to treat report preparation like a document-editing task, instead of setting up reports to be data driven. They’re used to gathering and typing information into a report by hand. If they discover errors, they must contact others to investigate and find a solution. This method relies heavily on human comprehension and attention. Finance and budget professionals typically take this approach because they don’t know how to use available tools and don’t have time to weed through instructional videos or “help” documentation. To them, manual manipulation seems simpler, safer, and even faster. It’s what they know. But in the long run, they will reap far greater benefits from doing the proper thing, rather than the seemingly simple thing. Instead of adding more steps to already complex processes, we challenge finance and budget teams to do away with unnecessary tasks. As their duties continue to expand, we invite them to think differently. A department that clings to manual data entry and manipulation is delaying the inevitable. Looking Ahead FHB intends to develop additional course offerings in the near future, following principles of adult learning to incorporate gamification and other interactive elements. For example, Workiva 201 will focus on advanced queries—how to write your own SQL (Structured Query Language) to extract every bit of available automation from the platform. Typically, writing SQL is left to members of an organization’s Information Technology (IT) staff because most accountants don’t understand the syntax. Unfortunately, in most cases, IT experts don’t understand accounting. This often leads to painful, time-consuming, back-and-forth communication in an effort to understand each other. We see massive benefits for those accountants who can bridge this gap effectively by fulfilling the more historic role of an accountant. A strong grasp of Workiva’s implementation of SQL will enable finance, budget, and audit teams to become less dependent on IT. We’re developing Workiva 101, 201, and additional courses because we know that a little incremental knowledge can unlock a world of understanding. And understanding brings competence, confidence, and calm. WORKIVA 101: BEYOND THE BASICS Course Description Have you taken Workiva’s basic training, but still feel ill-equipped to make use of its total functionality? Do you struggle to stay abreast of its newly updated features? Or are you strictly a Workiva beginner? Taught over two half-days, this live virtual learning opportunity is: Led by Workiva-certified experts Designed and delivered by CPAs, for CPAs Hands-on and interactive Our experienced course leaders will provide instruction, demos, and practice exercises designed to optimize your Workiva experience, covering: Understanding platform components Creating tables to hold any of the data you need Loading data into the database Creating queries using Workiva’s quick and easy builder functionality Connecting your data to spreadsheets Building spreadsheets and writing formulas based on the connected queries Creating document content and linking it back to the query-connected spreadsheets Built for Public Sector – Applicable for Corporate Users Too While the scenario we use as the context for the Workiva 101 training is a new GASB pronouncement, the training is just as applicable for corporate Workiva users. So users from any industry will come away with a more advanced understanding and practical mastery of this valuable software. Prerequisites: Be a currently licensed user of Workiva Have a workspace suitable for training Have the “Workspace Owner” role in the workspace to be used Complete Workiva Learning Hub course "Using Workiva" At the time of this article’s publishing, establishment of CPD/CPE eligibility for Workiva 101: Beyond the Basics is in process. Please check back in 1-2 weeks for updates. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Learn to do Workiva the FHB way. This hands-on course is designed by CPAs for CPAs and led by a Workiva-certified expert.

READ MORE