School District 83

- Rachel Raymond

- Success Stories

- minute(s)Time to Focus on the Big Picture: Automating Financial Statements for School District 83 Project: PSAB Automation Organization: School District 83 Students: 6,100 Platform: Workiva The Challenge The finance team at School District 83 (Okanagan-Shuswap, British Columbia) was looking to save time and money; reduce errors; and improve its reporting reliability, repeatability, and standardization; by automating its financial statements. When we met the team, their data preparation stage was heavily dependent on complex spreadsheets—requiring too much keying and leaving little time for analytics. “We utilized Excel, as well as other Office products—like Word for our financial notes and our financials, even discussion analysis. So, it was a very fractured overall process when we...look back on it,” said Jeremy Hunt, Finance Director for the district. The team was accustomed to finalizing, formatting, and preparing statements manually—a time-consuming and frustrating process. Additionally, they were required to complete Local Government Data Entry (LGDE) forms, which meant replicating the information from their annual report and manually keying it into the ministry’s template for online submission. Jeremy explained that in previous years, the team's work was paper-heavy. "We have binders. Nine-inch or 12-inch binders. I know they’re massive for year-end. And the backs of those…are all printed and messy,” he said. What’s more, the finance team frequently had difficulty finding original hard-copy source documents to back up their data. Jeremy looked forward to updating their process, so they “wouldn’t have to find a paper copy every year…that validates a number.” The district’s team also wished to collaborate simultaneously without risk of overwriting crucial information. “We wanted something that allowed access to the individual that was required to do that work, but locked down areas where we didn't want them working,” said Dale Culler, Secretary–Treasurer/CFO. They were also interested in a multi-functional tool. “The biggest limitation that we have in our department...is staffing resources to move forward with any initiative...and when we consider the end product, we wanted to move towards something that would allow us to potentially consolidate...future reporting requirements,” said Jeremy. The Solution FHB met with the district’s team to evaluate their existing processes and develop a customized solution to meet their needs. Initially, the conversation included using Caseware. “The Caseware discussion was because that's what we...were familiar with. But we also wanted to be open, to hear about advancements in the industry, where it's going...Caseware requires a very specific knowledge. We wanted something with the structure, the rows and columns that people are familiar with,” said Dale. In the end, FHB recommended Workiva. As a cloud-based platform, Workiva offers a collaborative database (Wdata) as a single source for data entry/management and an advanced report writer (Wdesk) for instant and automatic preparation of consistent, formatted reports—mitigating risk of data-entry and calculation errors and improving overall report accuracy. "It was concerning that it would be difficult to learn a new piece of software. But once we got into it and started to see the back end of it and how it really worked, and became more familiar with it, it was very Excel-based. That took away a lot of the reservations that I had, and I believe Dale had as well, about us being able to understand and use it in a logical manner that would follow what we're used to,” said Jeremy. The Service “Christine was on top of it. She kept us on the tracks…I can’t say enough about what she did for us. She’s very helpful.” –School District 83 Finance Director Jeremy Hunt Throughout the project, the School District 83 staff was highly impressed with the responsiveness of the FHB team. [FHB Principal Consultant Christine Gilbert, CPA, CA] did a great job…she would answer questions whenever I would throw them over, and…usually it was within like an hour,” said Jeremy. “It was a great experience.” “It's definitely appreciated that Christine had some experience in PSAB that we could draw support from,” he added. When asked to rate FHB’s general knowledge of Workiva and reporting standards on a scale of one to 10, with 10 being “the greatest ever,” Jeremy responded, “It’s a nine or a 10.” He wouldn’t hesitate to recommend FHB to peers and colleagues. “They were patient when we were struggling to keep up…they were accessible and worked with us on issues that we had…I would definitely recommend that FHB would be a good partner to implement any accounting-related software.” –Jeremy Hunt The Results So far, the greatest benefit of the Workiva implementation has been time savings. “It's just going to reduce the amount of…data entry that we have historically relied on. We were using reports from our old clunky system that doesn't provide great reporting…mapping was not the greatest previously. So, it's...going to speed up that manual entry time. It will help us validate data as well,” said Jeremy. Jeremy added that Workiva has far exceeded his expectations. “User friendliness has been amazing...it didn't take much training, to be honest, to understand how to use this product...on top of that, I can see how it links everything together and can easily produce something that is better than what we have previously done over many hours—in just an hour,” he said. Dale agreed, adding, “Workiva provides one place...in which to do review...and because it's very consistent with the way that we've been trained to look for things when...creating working papers, it'll be much quicker to do that." Before Workiva, "when things were disjointed...I’d have to interrupt...Jeremy...stop his workflow, so that he could show me where things were. In the new platform, I can just look at the progress of the review as it is...I don't have to wait for it to be finished; I can look at it live,” he said. Looking Ahead In light of this project’s success, District 83 has decided to move forward with two additional projects. “So…the bigger one is going to be the budget…we want to integrate our budgeting into Workiva,” said Jeremy. “We’re thinking next year, maybe toward the end of 2023, into 2024.”“...After this audit season, we’ll look at financial reporting quarterly…at some point maybe move into monthly statements,” said Jeremy. “Quarterly reporting is probably the next logical step...before we even do the budget,” said Dale. With all of the time they’ve saved, Jeremy looks forward to taking on higher-level tasks. “I'm fairly production-based right now in my job as a director, whereas I need to be more focused on oversight and the bigger picture,” he said. The District 83 team is pleased with how far they’ve come, and optimistic about the future. “We’re just scratching the surface of what Workiva can do for us,” said Jeremy. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

School District 83 wanted to improve and standardize its PSAB reporting process, making it more reliable, repeatable, and faster without increasing resources. They achieved that and more with the help of FHB.

READ MORE

GASB Statement No. 87 – Leases

- Amy Manthey

- Automating Financial Reporting

- minute(s)Did you miss the recent GFOA webinar on GASB 87 Implementation Guide? Here are the highlights… Effective Dates: The reporting requirements are effective for reporting periods beginning after June 15, 2021 and should be applied retroactively with prior periods restated as appropriate. GASB 87 will be effective for year ends of December 31, 2022, June 30, 2022, etc. Terminology: Previously, there were operating and capital leases. Now, there are “Leases” or “Leases under 87”. Under GASB 87, leases are considered a financing activity for the right to use another entity’s asset(s). GASB 87 defines specific reporting requirements for short-term leases and contracts that transfer ownership of the underlying non-financial asset. The definition of “short-term” remains as an initial term of 12 months or less, including any options to extend. Contracts that transfer ownership are identified by the transfer of ownership of the underlying asset at the end of the lease contract. The standard defines specific exclusions for leases for: Intangible assets Biological assets Inventory Service concession arrangement as defined in GASB 60 Paragraph 4 Underlying assets that are financed with outstanding conduit debt – unless both the asset and debt are reported by the lessor Supply contracts, such as power purchase agreements Lessee and Lessor value calculations are similar to each other as well as how the value was calculated for “capital leases." Lessee – recognize a lease liability and an intangible (right-to-use lease) asset at present value. Liability reporting is similar to how debt/financing is accounted for – which is different for full accrual versus modified accrual Lease asset value starts as the lease liability value, plus any payments made prior to the contract, less any lease incentives, plus any initial direct costs Lease asset amortization should be calculated based on the shorter of the life of lease or the underlying asset Re-measurement of lease only needed in specific circumstances Lessor – recognize lease receivable and deferred inflow of resources at present value (generally the same as the lessee amount). Deferred inflow is calculated at the beginning of the lease as the present value of lease payments less provision for estimated noncollectable amounts Subsequently, recognize deferred inflow of resourced and inflows of resources (revenue) over the term of the lease Subsequent periods amortization of the discount on the lease receivable and inflow of resources (interest revenue) is recorded Payments should first be allocated to accrued interest receivable and then to the lease receivable Lessor should keep underlying asset on the books Exception for leases of assets that are investments as defined in S72 and for leases that are subject to external laws, regulations or legal rulings (like Federal Aviation Administration) Note Disclosures: Lessee - The notes to financial statements should include a description of leasing arrangements, the amount of lease assets recognized, and a schedule of future lease payments to be made. Lessor – The notes to financial statements should include a description of leasing arrangements and the total amount of inflows of resources recognized from leases. Other items covered in GASB 87: Lease incentives Contracts with multiple components Contract combinations Lease modifications and terminations Sale-leaseback transactions Lease-leaseback transactions Intra-entity leases The Implementation Guide No. 2019-3, Leases is now available from GASB. Register for our Implementing and Automating GASB 87 Disclosures Webinar © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Effective for reporting periods beginning after December 15, 2019; the GASB 87 pronouncement changes the way leases are calculated and reported.

READ MORE

Answers to the 5 Big XBRL Questions

- Jamie Black

- Automating Financial Reporting

- minute(s)In Florida and California, XBRL is set to become a requirement for filing of your Annual Comprehensive Financial Report. If you are a finance officer in government, the term XBRL may be new to you. If you work in the finance department of a publicly traded corporation, you may have some familiarity with the term. This article answers the 5 biggest questions about XBRL for those in finance that will be required to utilize it and for those who have been required to file in XBRL but may not know a lot about the technology. 1) What is it? eXtensible Business Reporting Language (XBRL) was created by CPA Charlie Hoffman in 1998 as a way to transform business reporting. Sometimes referred to as "bar-codes for reporting," XBRL allows the facts which appear in a report to be "tagged" with a name which is centrally defined and managed. Those facts and tags can then be used to represent the contents of financial statements or other kinds of compliance, performance and business reports. In a typical finance department XBRL may be used to create, analyze and exchange financial reporting information including financial statements, general ledger information, and audit schedules. This allows XBRL encoded reports (called Instance documents) to be machine-readable. Inline XBRL (iXBRL) is a development designed to render the data in a visually appealing format. iXBRL takes the same data as an XBRL report and embeds it into an HTML document that can be viewed in a web browser. In other words, it is a way of tagging reports making them readable to both humans and machines. Since 2006 XBRL International has operated as the not-for-profit organization to "develop specifications to support the collection, sharing and use of structured data for data reporting and analysis". 2) Where is it used/required ? Today millions of XBRL documents are created annually in more than 50 countries and it is spreading into government in the United States: Passed into law in 2014, the Digital Accountability and Transparency Act (DATA Act) is a law that aims to make information on federal expenditures more easily accessible and transparent. It mandates that federal agencies report to U.S. Treasury using XBRL. More recently, the State of Florida is finalizing legislation that requires financial statements be filed in XBRL and meet the validation requirements of the relevant taxonomy. This will affect more than 400 Municipalities, all of which produce Annual Comprehensive Financial Reports today. This is set to begin for fiscal years ending on or after September 1, 2022. The State of Florida is likely to be just the first of many who adopt this legislation for greater reporting transparency. California introduced the Open Financial Statement Act, SB-598, in late February 2019. The proposed legislation would replace both the current State Controllers Office (SCO) report and the current PDF Annual Comprehensive Financial Report with iXBRL statements. 3) Why is it used? Currently, government departments submit their financial reports in a somewhat ad-hoc way within stated guidelines (Annual Comprehensive Financial Report/PSAB/OCBOA). The ability to compare and analyze how varying governments operate is essential to good decision-making and community planning. Aggregating and comparing the data from these reports from one organization to the next however can take countless hours. Even then, the flexible nature (professional judgement) of these reports can inhibit direct comparison. To better aggregate on an comparable basis, some states/provinces have attempted to solve the challenge more locally by requiring submission of another report (SCO in California / AFR in Florida / MFIR in Alberta / FIR in Ontario/ LGDE in British Columbia ). These reports can be directly compared and analyzed, but require lots of manual work both by local government to populate and the state/province to aggregate and analyze. This is what drives the requirement for financial information to be submitted in XBRL. It allows for standardized, apples-to-apples aggregation, analysis and comparisons by computers across multiple entities based on an industry-recognized standard. 4) How do I apply it to my Annual Comprehensive Financial Report? Some government finance departments use report automation software that enables generating iXBRL tagged reports. If this is your finance department, that's good news, as preparing reports in iXBRL format may be as simple as assigning tags to your documents. For those still using spreadsheets, XBRL will be more difficult and will involve engaging a 3rd party to do the tagging for you for a fee. A 2018 study by the AICPA & XBRL US on small reporting companies (not governments): Average price for XBRL preparation was $5,476 / year, 69% of the companies paid $5,500 or less annually, 12% of the companies paid annual costs of between $5,500 to $8,000 annually, 13% of companies paid more than $10,000 / year, Higher annual fees were due to complexities in their financial statements and rush charges imposed given the many last minute changes to the filings. Given the above numbers relate to small companies, we expect that fees for a government encoding a large, complex Annual Report would be on the very high end of this range. 5) When should I start working on this? The short answer is as soon as possible. If the rate of successful compliance with the 2014 Data Act is any indication, you will need significant time to get prepared. Whether you are required to file in XBRL already or are preparing for the day it is required, the time to begin preparing is here: If your current system supports iXBRL, begin planning to tag your Annual Comprehensive Financial Report with the appropriate XBRL taxonomy within the next year or so. If your current system is spreadsheet-based, you have a longer road to travel. We recommend you start by implementing a solution that automates your reporting AND allows for tagging your Annual Comprehensive Financial Report. You will benefit immediately from reduced workload and fewer errors. Then when XBRL reporting begins, you save again by avoiding 3rd party tagging fees. These savings alone could easily cover the cost of the reporting automation software. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

In Florida & California, XBRL is becoming a requirement for annual filing. If you are a finance officer in government, XBRL may be new to you. In this article we answer What is XBRL, Where is it used, Why it's useful, How do you apply it to your Comprehensive Annual Financial Report and When should you start tagging and testing.

READ MORE

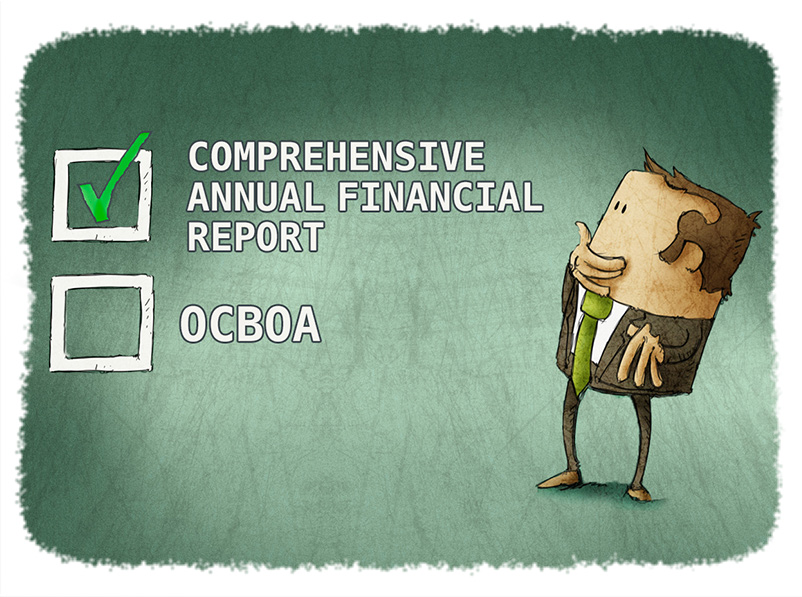

Why a Comprehensive Annual Financial Report beats OCBOA for school ...

- Jamie Black

- Automating Financial Reporting

- minute(s)If your School District prepares Other Comprehensive Basis of Accounting (OCBOA) financial statements, you are not alone. Preparing financial statements on this basis is the industry 'norm' in many states. But why? A growing number of School Districts are now preparing Annual Comprehensive Financial Reports (Annual Reports) for reasons that, when critically examined, are persuasive. This blog examines the differences between these two reports, the reasons why School Districts may opt for the lesser option and how to save time regardless of approach. Why is a Annual Comprehensive Financial Report better than OCBOA statements for School Districts? The Association of School Business Officials International (ASBO) cites four key reasons: Demonstrates that your district is committed to transparency and accountability. Makes district financial information more accessible to all members of the school community. Is viewed as a positive decision-making factor by credit rating agencies. Can be useful for meeting continuing disclosure requirements for bonds. Given the above, why do so many school districts still choose to prepare OCBOA reports? It is simple. They are easier for a lay-person to understand and easier for finance to prepare. The Annual Report is undeniably a more complex, time consuming report (both to prepare and to understand). In many ways the extra level of complexity is the underlying reason that it is a more accurate and useful report. Many school district finance departments are stretched to capacity with their current workload and may feel they just don't have the capacity to tackle an Annual Report. If you are like many other finance professionals who say the benefits of the Annual Report do not outweigh the extra work, there is another element to consider: Automation. If you are using spreadsheets and word processing tools to prepare your OCBOA reporting today, converting to an Annual Report while simultaneously implementing a report automation tool will likely reduce total workload below your current levels. Bonus tip: Implementing report automation tools with your OCBOA reporting (should you resist the urge to change) will save you a ton of time too! Conclusion It is more difficult to produce the Annual Report, but the right technology will allow you to have the best of both worlds - world class reporting without department-breaking time investment. Get started today. Here are some great resources: ASBO Certificate of Excellence in Financial Reporting Resources. A guide for what to demand in your Annual Report automation solution. Note - these requirements will apply for automating your OCBOA reports too! © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

In many states, lots of school districts issue OCBOA statements, not Comprehensive Annual Financial Reports. In our article, you will learn why OCBOA statements are so popular, four reasons an Annual Report is better, & how to produce an Annual Report with less work than OCBOA statements.

READ MORE

Lipstick on a Pig: 6 Spreadsheet-based Financial Reporting Tool Flaws

- Jamie Black

- Automating Financial Reporting

- minute(s)You may be familiar with the expression "Lipstick on a pig". Variations of the expression date back nearly 130 years but the meaning has not changed; Superficial improvements that do not change the underlying nature of something. Spreadsheets by any other Name We have seen an increasing number of spreadsheet-based reporting automation tools promoted as ultimate solutions for Comprehensive Annual Financial Reports & Budget Books. This is ironic considering many organizations are using spreadsheets today and are looking for a better approach. Sometimes these solutions are desktop add-ons to enable better connections to a source of data. Sometimes these are cloud-based solutions that rely on spreadsheets to maintain their data and develop their reports. Hard to Tell They are Spreadsheets The fact that these are spreadsheet-based tools may be hard to tell on initial review. You can spend hours reviewing their websites and sitting in presentations and still not recognize it. It's not surprising they don't advertise their reliance on spreadsheets given the scientific evidence of their weaknesses and the numerous stories of very public disasters caused by spreadsheets. The Lipstick In fairness, these tools often have improvements over the desktop spreadsheets you are used to, such as: Better collaboration abilities for sharing comments, tracking changes or assigning tasks. Better audit trails and change management. Ability to tie supporting documents to a given value / cell. More granular security / permissions. The Pig But the core of these products are still spreadsheets. That means they suffer from the traditional spreadsheet weaknesses: No database - All data resides in spreadsheets / workbooks not in a database. This means you must build all your own personalized systems to: ensure your G/L balances identify the 100 - 1000 new G/L accounts added each year No processes/workflow - There is no structured system that you can leverage to support industry best practices. What steps should be followed and in what order? You must develop all of these processes on your own and maintain them separately from your reporting environment. No grouping mechanisms - The G/L accounts that sit in your spreadsheet must be summarized in numerous different ways (by object, by fund etc.) to power your Comprehensive Annual Financial Report or Budget Book. If you use spreadsheets, formulas must add the right accounts together. This is fragile and susceptible to error. Moreover, unless you interrogate every formula, there is no way to know what is being included in a given number; there is no legend. Assuming you do get this right in year one, all the new accounts next year means these formulas must all be updated. Tons of custom formulas - All values are derived by "linking" - which is to say writing spreadsheet formulas of varying complexity. Any mistakes you make means errors in your report. Consistency in how these formulas are written or maintained is entirely dependent on the user's expertise, accuracy and completeness. No content libraries - Reporting standards are continually evolving. There are new GASB pronouncements all the time and keeping up with them and what new statements, schedules or footnotes are required this year can be daunting. Spreadsheet solutions do not come with any content. It is entirely up to you to figure out what must be presented and how. No adjusting journal functionality - Adjusting or changing balances is an absolute requirement for financial statement /Comprehensive Annual Financial Report production. In spreadsheets you are left with no tools for the following: The values in your G/L are typically maintained on a modified accrual basis. For many of your statements, you need full accrual. Debit balances in A/P accounts or credits in A/R are just two examples of balances you need to reclassify. Prior year adjustment / restatement caused by changes in accounting policy. Our message in this post is not that the additional features - the "lipstick" - have no value, or that there is no situation when spreadsheets should be used. We are saying that when finance & budget officers evaluate possible solutions for their most complex reporting tasks (Comprehensive Annual Financial Reports & Budget Books), they must exactly match the critical requirements of their processes to the solution's abilities. If they do this carefully, they will find that spreadsheet-based "solutions" are only marginally better than their own collection of desktop-based spreadsheets. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Comprehensive Annual Financial Reporting and Budget Book tools based on spreadsheets are all the rage. Don't overlook their considerable weaknesses.

READ MORE

Budget Book VS. Financial Statements: What's Worse?

- Jamie Black

- Automating Financial Reporting

- minute(s)Finance professionals in government and education have several daunting (frustrating, annoying, I could go on..) reporting challenges to address each year: the Annual Audited Financial Report, the Budget Book and some special purpose reports like the FIR for governments in Alberta & Ontario or the CAUBO report for universities & colleges While automating the annual financial statements is generally recognized as a major win for your finance team, perhaps an even bigger win is automating the budget book. To an outsider, this might be a surprise. Isn't going through an audit the worst thing possible? Admittedly, it's not a lot of fun and yes it is incredibly time consuming; but the budget book is worse. Here's why.. 1) Much more content How long are your annual financial statements? For many of our clients (governments, universities & colleges, large publicly traded companies) a typical set of statements include: a cover page a table of contents 4 statements 20 - 30 notes 4 - 6 schedules All told, the report is perhaps 30 pages. For a regional district or a local government in the USA that must prepare a Comprehensive Annual Financial Report the page count is likely to increase to 200 + pages. In any case, there is a lot of complexity to these reports. A budget book (sometimes called the "financial plan") is almost always much larger. 200 or 300 pages is actually a small budget document. For those clients that participate in the GFOA Distinguished Budget Presentation Awards program, their guidelines tend to result in very large budget books. Some even approach 1,000 pages! All of this content means more work. More tables, more text, and more numbers that must reconcile. 2) Considerable emphasis on non-financial data For the most part, financial statements are focused on financial data. There are text portions (the policies and notes), but even then they are either relatively static (e.g. your revenue recognition policy is not changing year-by-year) or primarily about details of the financial data. In contrast, it is very common for the budget book to contain hundreds of pages of narrative. Large narrative discussions of the following are required of GFOA Distinguished Budget Presentation Award Program participants in a budget book: the budget process, entity-wide long-term financial policies, organizational charts and descriptions of the organization, its community, the population and background information related to the services provided. Why does this make the process harder? More content means more page breaks, larger table of contents, more pages to number etc. In short, it means more elements to have problems with. Secondly, much of this narrative changes year after year, necessitating a process of collecting, organizing and updating hundreds of pages of content. 3) Graphs & pictures Annual Financial Statements rarely include graphs & pictures. They tend to be very utilitarian documents, comprised almost exclusively of tables of data and a few pages of narrative in the notes section. Very few of our clients even add a logo or picture to the cover page! Contrast this with the budget book. The vast majority of these documents contain many graphical elements including: organization charts graphs pictures of ongoing projects, the finance team, local wild life etc. A quick review of one of the budget book for one of our clients showed that in the 425 pages, there were nearly 300 graphical elements! Just like the challenges listed above in large narrative sections, graphical elements must be managed and updated year after year. To make matters worse, consider that many finance professionals are not expert in how to use graphical elements to maximize communication effectiveness. 4) A much broader collaboration In most organizations, assembling the annual financial statements is primarily the task of the core finance team. While dozens of folks may contribute reconciliations and supporting documents, perhaps only a handful of people contribute to the statements directly. For the budget book, dozens or even hundreds of people contribute to that huge volume of text we mentioned earlier. It might only be a few paragraphs per person, but it seems like every Tom, Dick & Wendy contribute to the budget book content. That means the team that assembles the book needs to track who is contributing to each section. Then they need to know if that individual provided their content yet, and when they do provide the content someone has to make sure that it gets reviewed, approved and finally correctly inserted into the end report. That is a lot of little steps which must be repeated potentially hundreds of times to arrive at the completed book. The End Result The end result of these four points is one absolute fact. If your budget document is hundreds of pages bigger than your financial statements, budget book automation will be an incredibly valuable accomplishment for your organization. © 2025 FH Black Inc. All rights reserved. Content may not be reproduced, excerpted, distributed, or transmitted without prior written consent.

Budget book automation provides massive value for universities & governments by reducing time investment, eliminating errors & more. Here's why...

READ MORE